Spending in the Time of COVID: A Love Story

Why the pandemic didn't tame our love of spending money, but may still positively change our financial habits in one important way

In this edition of The Root of All, I write about something the pandemic has motivated many people to do and which has been shown to improve financial success. Also in this edition, a very special guest answers the On the Write Side of Money questionnaire: J.D. Roth, creator of the popular personal finance site, Get Rich Slowly.

If you enjoy this, please consider joining hundreds of other like-minded readers by subscribing to The Root of All. It’s free!

As most people have mentally gotten over COVID, so too have we gotten over one positive contagion that spread during the pandemic. Let’s call it “frugal fever”, the symptoms of which included canceled gym memberships and home-cooked meals.

Did you catch it?

It’s not surprising our spending habits dramatically changed as a result of lockdowns and pandemic-related restrictions. We spent less money on things like transportation, dining out and clothing. What’s interesting is that we cut our spending – and discovered that we liked it.

A paper from the European Central Bank analyzing consumption habits during the pandemic said “many households report ‘not missing’ what they cut back on during lockdown – even after restrictions are lifted.” “Not missing it” was the second most cited reason for spending less on products and services in France, Germany and the Netherlands, behind only the risk of coronavirus infection.

Meanwhile, a 2021 Northwestern Mutual study found 95% of U.S. adults said they adopted better financial habits as a result of the pandemic and expected to maintain those habits going forward. The top financial behavior adopted, as mentioned by 45% of respondents, was “reducing living costs and spending.”

Americans also started to rethink how much money they needed to be wealthy, achieve financial happiness and feel financially comfortable. According to Charles Schwab’s 2021 Modern Wealth survey, Americans said the average net worth it took to be wealthy was $1.9 million, which was significantly less than the pre-pandemic amount of $2.6 million.

The embrace of a more frugal lifestyle made some economists and researchers think the pandemic might permanently alter our spending habits.

This was good news. Many people just don’t save enough money. Half the country doesn’t have enough saved for retirement and nearly two-thirds can’t afford a $1,000 unexpected expense. Not to mention the adverse environmental impact of consumerism.

It was nice while it lasted

Alas, the idea of a permanent shift toward frugal spending habits seems to be nothing more than wishful thinking, like the belief COVID would simply disappear in the summer heat. Once pandemic restrictions were fully lifted, our love of spending money returned with the swiftness of someone breaking their New Year’s resolution diet on February 1st.

This is shown by the latest survey numbers for 2022.

The percentage of U.S. adults who say they’ve adopted better financial habits: declined to 73% from 95%.

The percentage of U.S. adults who say “reducing living costs and spending” is their top financial behavior: declined to 35% from 45%.

The amount of money Americans think it takes to be wealthy: increased to $2.3 million from $1.9 million.

Despite high inflation and fears of a recession, personal consumption has been up for much of 2022. At the same time, entertainment and hospitality companies like Disney and MGM have recently reported record earnings as people flock to theme parks and casinos.

Why frugality didn’t survive the pandemic

Put simply, the pandemic didn’t make us more frugal.

It turns out that external forces, such as an economic crisis, generally don’t permanently change our financial habits. Even the Great Depression, which is often mythologized as traumatizing people into extreme frugality. We’ve all heard stories of older tightfisted family members who, scarred by Depression-era bank runs and wartime scarcity, diligently saved every dime in a jar or under the mattress. But that’s more fiction than fact.

As David Brooks wrote in a 2000 essay, “this morality tale doesn't hold up to scrutiny… there's no pile of evidence to suggest that the Greatest Generation, as we now worshipfully call it, is reacting differently from anybody else… In fact, the members of this supposedly thrifty cohort are setting new standards for post-retirement consumption.”

Brooks reported that the Bureau of Labor Statistics' Consumer Expenditure Survey showed that people aged 65 and older increased their spending more than any other age group between 1987 and 1997. They even spent more money on entertainment than households run by 25-year-olds. Moreover, the market research firm Claritas found they preferred buying Cadillacs and Lexuses rather than Fords and Hondas.

When times are tough and we’re forced to make involuntary choices, we tend to only adjust our spending habits temporarily. To change our spending habits permanently, especially in a country as individualistic as America, it has to be voluntary. Because changing our financial behaviors and attitudes is hard to do.

For one, spending money gives us pleasure – at least momentarily. The boost of happiness we get from buying something convinces us to keep spending to retain that same level of pleasure. So, we continue to strive for more – cars, homes, TVs, clothes, etc. This is what psychologists coined the “hedonic treadmill”.

One way off the hedonic treadmill is through sheer willpower, which may be in short supply as the result of the pandemic. Research suggests our willpower works like a muscle; it gets tired when overworked. A study published by the B.E. Journal of Economic Analysis & Policy indicated that lower-income shoppers use more willpower than richer shoppers because they have to exercise more control over their spending decisions, which then makes them more likely to eat and drink while shopping. Devote willpower to one set of difficult decisions, you deplete willpower in other areas.

After the constant bombardment of difficult health decisions – wearing a mask, practicing safe distancing, washing hands – we may not have the willpower to keep our spending in check. We’re exhausted from running the pandemic treadmill and want some retail therapy.

How the pandemic may improve people’s financial lives

After a yearslong confrontation with our own mortality, who’s motivated to live a more restrained, frugal life anyway? Life’s too short.

The story of Ronald Read, a humble and extremely frugal janitor who died a multi-millionaire, is often used as an anecdote to show how almost anyone can build wealth by living within their means. Certainly, his story is a testament to the benefits of saving and investing. But he didn’t travel much and wore an old coat kept together with safety pins. That doesn’t sound like what many of us would consider a well-lived life. Surely, a portion of his $8 million nest egg could have been used to buy a new coat.

Unless the main thing you cared about was donating millions of dollars to support the local hospital and library you valued most, which is what Read did.

Isn’t that the highest purpose of money, to support the things you love and value most in life (authenticity, family, charity, travel, financial independence, etc.)?

I think it is, and I think that’s where the pandemic could ultimately leave a lasting impression on our financial habits. Although the pandemic hasn’t directly changed our spending habits, it has motivated us to make changes in our lives that can improve our financial success indirectly.

Here’s how:

Many people struggled — and continue to struggle — financially, physically and mentally as a result of the pandemic. But overall, the pandemic has been a time to review our lives and think about what life could look like moving forward. However, it may be more accurate to say the pandemic has been a seismic earthquake so rattling it has forced us to reevaluate our priorities and reckon with our values.

Over the past two years, we analyzed what we do, how we work, where we live, who and what we love. Then, we’ve made big and small decisions based on newly established personal values: we moved, we pursued new job opportunities, we started businesses, we volunteered and donated, we put on running shoes for the first time, we formed and severed relationships, we read thick classic novels, we baked bread.

Studies suggest that life-threatening events, like natural disasters, often motivate us to make take life-altering actions. When confronted with highly challenging life circumstances we can’t control, we tend to look inward. As Austrian psychiatrist and Holocaust survivor Viktor Frankl put it:

“When we are no longer able to change a situation, we are challenged to change ourselves.”

These moments for renewal that arise out of the ashes of disruption are what Wharton School professor and author Katy Milkman call “the fresh start effect”. In a sense, the pandemic has become an opportunity for a fresh start — to make meaningful changes out of adversity and find a new sense of purpose.

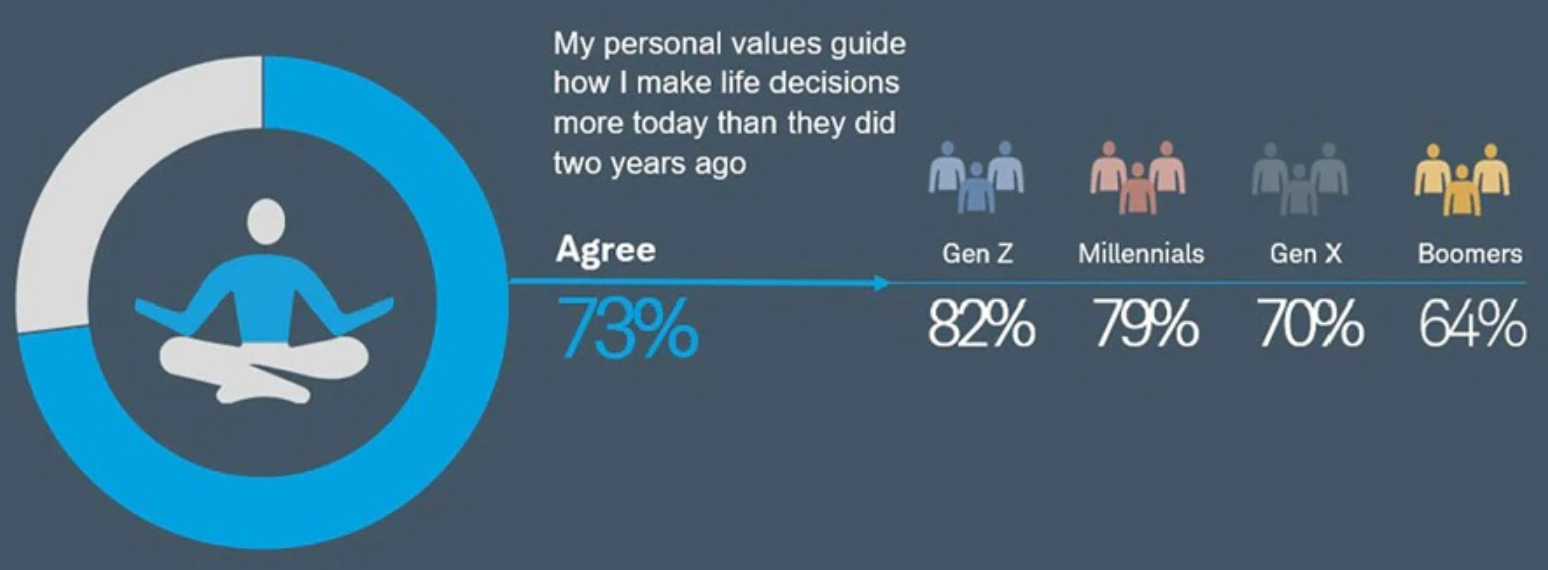

Consider the 2022 Charles Schwab survey mentioned above found nearly three-quarters of Americans (73%) say their personal values guide how they make life decisions more today than they did two years ago. And, more than 80% say those personal values influence how they manage their finances.

Such a clear sense of purpose and understanding of one’s personal values can lead to greater financial success.

A study published in the Journal of Research in Personality shows that people with a higher sense of purpose had higher levels of household income and net worth. They were more likely to make financial decisions that supported their long-term goals and personal values rather than waste time and money on immediate, impulsive decisions.

Financial success begins with purpose.

It echoes the sentiment of American naturalist and essayist Henry David Thoreau who famously put himself voluntarily in COVID-like isolation along Walden Pond in Massachusetts.

Of his experience he wrote:

I learned this, at least, by my experiment: that if one advances confidently in the direction of his dreams, and endeavors to live the life which he has imagined, he will meet with a success unexpected in common hours.

What he means is that to live the life you imagine starts with clear intentions (or values). And, when your actions align with your intentions, you will successfully achieve your dreams and goals.

For many people, the pandemic has kickstarted this process.

Coda

So, while the pandemic didn’t curb our love of spending money, it very well may lead us to develop the habit of spending with greater intention to make the most of this one wild and precious life, to quote poet Mary Oliver.

Consider one thing a lot of people spent money on during lockdown: a Peloton bike. It offered an outlet to stay connected with others, stay healthy, stay sane and stay motivated by the likes of star instructor Robin Arzon, who proposed this question:

“To the days you haven't lived yet, what could go right?”

It’s a good question to ask ourselves, one that can help guide us now in how we spend the rest of our lives – and our money.

On the Write Side of Money

A short Q&A with notable finance/business writers about writing.

In this edition, I’m honored to welcome the one and only J.D. Roth. For the unfamiliar, he’s who I would consider as one of the Godfathers of personal finance blogging, having started his popular website Get Rich Slowly in 2006. His writing is both deeply personal and informative — and his responses below reflect that. Enjoy!

(Full disclosure, some answers have been lightly edited for brevity purposes.)

Describe your ideal writing experience (ex. when, where, what, how).

I have ADD, which isn't good for a writer. Even slight distractions and interruptions can derail me drastically. So, my ideal writing experience is: I'm isolated with nothing to interrupt me and nothing else on my schedule to make my mind worry. I'm tackling a specific task and working at it until completion.

In practice, this can take a couple of forms. At this very moment, I'm on a five-hour flight to Orlando. Great! This is a perfect writing environment: Taylor Swift on the headphones, writing in progress (email, in this case). I also like going to the public library and recreating the same environment: headphones, nothing on my calendar, laptop open and writing. It's difficult for me to do this at home.

What led you to start writing?

I have always been a writer... or so it seems. In reality, I'm a writer because my parents and teachers gave me lots of positive reinforcement when I was a kid. In second, third and fourth grade, adults praised me for my kid-sized stories. This led me to want to write more. And the more I wrote, the more praise I got, so I stuck at it.

By the time I got to college, I'd had 10 years of people giving me positive feedback on my writing. This made me very interested in pursuing it as a career. I just never imagined that I'd end up writing about personal finance on the internet (because there wasn't any internet when I was in college!).

What trait is most important to become a good writer?

The most important to become a good writer is simple: Write. Write all of the fucking time. I talk to a lot of people who say they want to become writers, but they don't ever write. They just talk about it. If you want to be a writer, you have to write. More than that, you have to share your writing with other people, and you can't be precious about it.

You can't get hurt feelings when somebody says, "I didn't like this" or "you should do this differently". Listen to all feedback. You don't have to accept it necessarily, but listen to it and, when appropriate, incorporate the advice into the way you write.

For me, it has been valuable to work with professional editors. Editors hack the hell out of your work, and they help you to see that ultimately a written piece is a product. You're trying to accomplish something with each article or book or play you write, and if you're not accomplishing that, then you need to make improvements.

But really, the most important trait to become a good writer is to write all of the goddamn time. Understand that maybe 90% of what you write will be shit, and that's okay. Your good stuff is built on a foundation of your bad stuff.

How do you judge if a piece of writing is successful?

A piece of writing is successful if it communicates what you intended to communicate. If readers understand the message you were trying to convey, you've succeeded. If you meant to be funny and people think you were funny, that's success. If you want your audience to take action and they take action, that's success. If you want people to question their beliefs and they do, that's success. A piece of writing has failed when your audience doesn't get the message you were attempting to send.

Who are your favorite writers?

This is going to sound crazy, I know, but my favorite writer at the moment is Taylor Swift. I'm not joking. She's both prolific and passionate, and these qualities are reflected in her body of work. It's been fascinating to watch her talents mature as she ages (she's only 32 years old!). She's gone from writing songs about teen angst to tackling tougher subjects. But my favorite Swift songs tell stories. Her album "Folklore" has several of these, and they're great.

It's much more difficult to nail down favorite traditional writers. I like most writers to some degree or other.

That said, some of my favs include James Thurber (it's difficult to write humor, but Thurber was able to do it well), Patrick O'Brian (whose Aubrey/Maturin sea tales are magnificent), Mary Stewart (whose Arthurian books have a sort of poetry to them), Ursula LeGuin, Alexander McCall Smith, and Yuval Noah Harari.

Favorite books include "True Grit" by Charles Portis, "The Power of One" by Bryce Courtenay, "The Crystal Cave" by Mary Stewart, "House of Suns" by Alastair Reynolds, and "The Unbearable Lightness of Being" by Milan Kundera.

What writing book, article or blog has helped improve your writing?

All books help me improve my writing. I'm not joking. Earlier I said that the most important trait of a writer was to write. Well, the next most important trait is to read. Reading allows you to see the product of other writers.

But as for one book? I think that William Zinsser's "On Writing Well" probably had the greatest impact on my own writing. I'm not saying that it's the best writing manual, but it was the best manual for *me* at the time that I read it (around 2007). It helped me to become a much better writer.

What money book, blog or podcast do you recommend most?

Honestly, the book I recommend most is "I Will Teach You to Be Rich" by Ramit Sethi. It's an excellent overview and introduction to personal finance with solid advice throughout. I also recommend "The Simple Path to Wealth" by J.L. Collins. A recent fav that I think I'll end up recommending a lot is "Designing Your Life" by Bill Burnett and Dave Evans.

The blog I recommend most is Raptitude by David Cain.

What are your favorite sources for news, research, data, etc.?

This is a tough question to answer. I'm not sure I have favorite sources. The modern web has become a cesspool of ads and SEO and bullshit. But that's a rant for another time. The net effect is that there aren't any terrific sources of info anymore. They're all flawed in some way.

That said, I actually quite like the U.S. government websites as a source of information. I'm talking about sites like the Census Bureau and the I.R.S. and quasi-governmental agencies like the Federal Reserve. These sites have lots of excellent info presented in interesting ways.

I also like aggregators. There aren't many of these left (although Jim Wang and I run one at Apex Money). Perhaps my favorite and most-used aggregator is Abnormal Returns. Dude (Tadas Viskanta) does a terrific job of curating interesting articles.

You’re organizing a dinner party. Which three people, dead or alive, do you invite?

If I were organizing a dinner party, the top person I'd invite is Taylor Swift. Swift is a fantastic writer, musician, and entrepreneur. She kicks ass. Plus she's a dork. I'm a huge fan and would love to talk with her about her work.

The second and third guests are more difficult to figure out. I guess number two would be my cousin Nick, who died earlier this year. Nick was also my best friend and I miss him. Plus, I have some questions about his stupid estate — haha!

Number three would be the Buddha. Would love to get his thoughts on modern life. (And this isn't relevant to anything, but I just realized it would be HILARIOUS to have a rock musical about the life of the Buddha in the same vein as Jesus Christ Superstar. OMG. This idea is so funny.)

What is your favorite piece of advice (writing, life, finance or business)?

I have several favorite pieces of advice, but one I come back to frequently is this poem/quote/saying from Hafiz: "The small man builds cages for everyone he knows while the sage, who has to duck his head when the moon is low, keeps dropping keys all night long for the beautiful rowdy prisoners." I like this so much that I had a friend paint this for me:

This quote encompasses my life philosophy. This is my aim. I'm out there trying to drop keys so that other people can set themselves free.

Take a Penny, Leave a Penny

Links to various things I enjoyed recently. Feel free to share with me what you’ve been reading, either in the comments or at rootofall@substack.com

The Steve Jobs Archive (This is really cool… would love to see similar sites of other historical figures)

I love and admire my species, living and dead, and am totally dependent on them for my life and well being.

Your Career Is Just One-Eighth of Your Life (Derek Thomson always with words of wisdom)

Work is too big a thing to not take seriously. But it is too small a thing to take too seriously. Your work is one-sixth of your waking existence. Your career is not your life. Behave accordingly.

We're Not Good Enough to Not Practice (Kiese Laymon)

Be driven. Be curious. Write to connect. Write to explore. Write to make sense of that which you don't know or remember. Write to discover. But never think something is good just because you wrote it.

Your Moment of Grace

"Life is trying things to see if they work."

-Ray Bradbury