Managing Your Personality in Your Portfolio

Whether we can admit it or not, the way we invest is heavily influenced by our personalities.

As I struggle with the hardest Dry January in history, I’ve thought a lot about people I’ve known who could freely indulge in alcohol or drugs yet still meet all life’s obligations. They always made it to the party, always confidently got behind the wheel, always woke up the next morning in their own bed, always kissed their spouses and children goodbye and made it to work on time…

…until the time they failed to see the on-coming headlights.

How does someone remain oblivious to risk and live under the presumption of good outcomes? I suppose it’s easy when that’s all you know.

I can’t say the stock market, cryptocurrency or anything else is a bubble right now. But I can say a lot investors seem oblivious to the potentially adverse consequences that lie in wait. New brokerage accounts are at an all-time high and TikTok investing videos made by teens attract millions of views.

Insurrection. Pandemic. Millions unemployed. Killer hornets. The cancellation of Caillou. Still the market marches on. The party continues.

Considering the historical events that transpired over the past 12 months, it’s hard not to feel uneasy about the unperturbed rise of the stock market. Except, what do your feelings matter anyway? As Josh Brown said about the callousness of investing in a recent podcast: “The stock market doesn’t care how you feel.”

He’s right.

However, you should care how you feel. It’s worthwhile to ensure you make investment decisions for the right, rational reasons, rather than chasing hot stocks or following the herd. Because eventually your luck can run out.

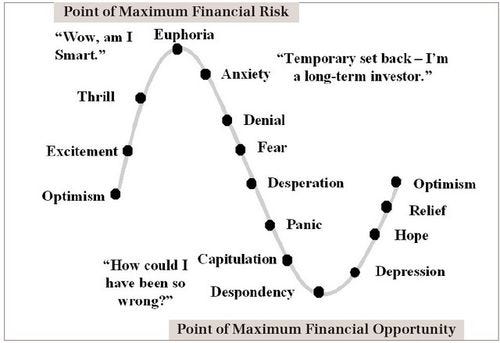

The Stock Market Mirrors Our Personalities

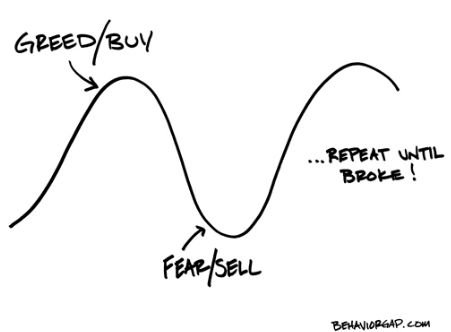

The stock market is propelled by tides of greed and fear. This concept is a famously illustrated in line charts people often share when the market hits an all-time high or sharply declines.

It’s easy for an investor to say that’s not me. I’m smarter than that. I have my emotions in check.

But it may be more accurate than we’ve realized, as our personalities seem to operate on the same undulating trajectory.

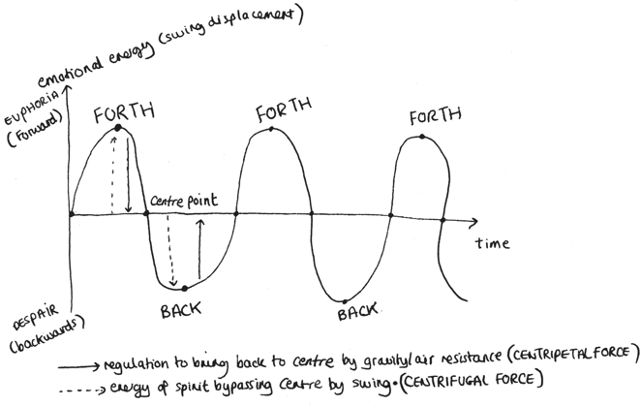

Look at this illustration from Dr. Camilla Pang, a postdoctoral scientist in bioinformatics, who recently published the book, An Outsider’s Guide to Humans: What Science Taught Me About What We Do and Who We Are.

Dr. Pang compares our personalities to a playground swing, oscillating between euphoria and despair. The extent of those highs and lows depend on the amplitude of our personalities.

She writes:

Just like people, oscillators can be predictable and they can be unpredictable. They have an expected path to follow, but one that is subject to change depending on the external forces being exerted on them: in the swing example, you might drag your feet on the ground, creating friction, or propel yourself outwards, revving into a salient rhythm. And, just as our personalities can be subdued or extreme, oscillators can have amplitudes (peaks and troughs of their arc) that are spiky or shallow.

Because just as, on the swing, we are quite literally riding a wave of simple harmonic motion, our lives and personalities have their own inherent wave patterns.

Think of the people you know who always seem to be in control of their emotions, never get overly bothered by problems and are essentially “steady.” That is a low-amplitude personality, one which never departs too far from its resting equilibrium. Neither the emotional forces propelling this person nor those dragging them back are ever too great. This is a slow, steady, smooth ride on the swing: no sudden jerks or motion sickness.

By contrast, a high-amplitude person is someone with more energy to burn, whose emotional peaks and troughs are more extreme, and who is also probably traveling faster—at a higher frequency. This is the kind of ride on the swing that can make you feel sick, as the soaring highs are tempered by unsteady downswings and sudden jolts of force when you’re not expecting it.

Whether you are a high- or low-amplitude personality—and both have their strengths and weaknesses—it’s important to understand the rate at which your temperament swings… To make our progress through life as natural as the “good” ride on the swing, we need an understanding both of our own amplitude and that of the people around us.

Many investors today are riding on the cusp of a mental peak, unaware like a functional alcoholic of the risks not realized yet, when everything swings the other way.

Some self-awareness can help you strike a balance between high and low, risk and safety, for smooth, steady progress toward your financial goals. It can help you avoid taking unnecessary risk and following the herd mentality of the market.

Investing on emotion is not a good investment strategy. Credit John Maynard Keynes for arguably the greatest investment quote ever: “Markets can stay irrational longer than you can stay solvent.”

Managing Your Personality When Investing

Conventional finance wisdom says you can control your emotions or change your way of thinking. But that is difficult to do. As an article from the University of California, Berkley explains, “…once our minds are made up on important matters, changing them can be as difficult as stopping a train hurtling at full speed, even when there’s danger straight ahead.”

The good news is that we are not at the mercy of our personalities. There are several ways to manage -- or neutralize – our personalities within our portfolios.

One common option is to automate your investment process as much as possible. For those saving in an employer-sponsored account, contributions can be automatically deducted from your paycheck. This is a form of dollar-cost averaging. You invest every month regardless of what the market does. You can also automate your asset allocation by investing in a target date fund. Although target date funds are not perfect, they beat picking funds randomly or based on past performance, or not investing at all.

True, that guarantees you’ll never become an overnight market whiz millionaire.

So, if you are overwhelmed by the desire to speculate on the market, there is no harm in to creating a “play fund” separate from your retirement funds. Consider this a speculative account that has no bearing on your long-term investment objectives. The Wall Street Journal’s Jason Zweig recently recounted the timeless warning of Benjamin Graham to “Never mingle your speculative and investment operations in the same account, nor in any part of your thinking.”

Instead of getting mixed in with the investment flavor of the month, a diversified portfolio of cheap index funds is likely to better serve you over the long run. A classic study, “Determinants of Portfolio Performance,” found asset allocation choices accounted for most of a portfolio’s return, not by market timing or security selection.

Of course, your personality may make it hard to stay the course over the long run.

Perhaps then, the most effective option for you is to work with a financial adviser. Essentially, it is akin to putting a human buffer between you and your portfolio. One the primary roles of a financial adviser is to act as an objective voice of reason. With most financial advisers you can give them discretion over your investments based on the policy agreed to at the start of your relationship. Before making an investment change, you can speak with a professional to discuss your thoughts and feelings in the moment.

There’s no shame in handing over the keys to your portfolio if it is in your best interest.